Three ways to get to integrated thinking: lessons from Australia

Integrated reporting is a means to an end – and the end is not necessarily the publication of a single performance report that combines financial reporting and sustainability disclosure. Rather, the process that sits behind integrated reporting is meant to instill integrated thinking within a business. Integrated thinking supports decision-making and sustainable resource allocation by encouraging an organisation to consider how it uses and affects financial and nonfinancial resources in its operations. Integrated thinking is borne from integrated reporting because developing an integrated report requires an organisation to consider not only how it has created financial value, but also how it has created, preserved, or eroded other forms of value (human capital, natural resources, business relationships, intellectual capital, and the like). As a resource for integrated thinking, see the Value Reporting Foundation’s recently published Integrated Thinking Principles.

The Integrated Reporting Framework (<IR> Framework) is the flagship resource for organisations looking to embark on integrated reporting. Anyone who has managed an integrated reporting process will tell you that integrated reporting is a journey, and an organisation should not expect to achieve full compliance with the <IR> Framework immediately. Instead, the <IR> Framework guidance can be used flexibly to accommodate the particular circumstances of an organisation.

Several jurisdictions around the world have recognised the value of integrated reporting and the <IR> Framework. In Australia, the ASX Corporate Governance Principles and Recommendations (Fourth Edition) state that the principles of integrated reporting can be used by companies when preparing existing statutory reports. Furthermore, Australian excellence in integrated reporting has been recognised by the Australasian Reporting Awards, which has presented a Special Award for Integrated Reporting for several years.

Buoyed by regulator and industry encouragement, several listed companies in Australia have begun their integrated reporting journey. The rest of this article steps through ways that Australian companies have used the <IR> Framework to instill integrated thinking and meet expectations for stronger connectivity between financial reporting and sustainability disclosure.

Visualize how your business creates value

An integrated report all starts with the company’s business model – which according to the <IR> Framework can be defined as “its system of transforming inputs, through its business activities, into outputs and outcomes that aims to fulfil the organisation’s strategic purposes and create value over the short, medium and long term”. Articulating a business model can be a complex task, however, even before considering how it relates to its external environment. In fact, one-third of reports reviewed by the Alliance for Corporate Transparency didn’t disclose a business model at all.

Australian examples have tackled the business model challenge by creating visualizations that map out the logic of their activities and their relationships with financial and nonfinancial resources:

- The National Roads and Motorists’ Association’s business model visualization in its 2021 Annual Report positions the business within the context of its environmental externalities, while illustrating the connection between inputs, outputs, and value creation outcomes

- CPA Australia’s business model visualization in a supplemental document to its 2020 Annual Report shows the logic of how its strategic goals link to outcomes according to the <IR> Framework’s six capitals, while also showing societal impact through the UN Sustainable Development Goals

- Dexus’s business model visualization in its 2021 Annual Report shows how the business “transforms” its inputs into value for itself and its stakeholders, and also identifies “value drivers” for each value creation outcome – such as waste management for environmental outcomes and professional development for human capital outcomes.

Structure the report by stakeholder outcomes

The six capitals of the <IR> Framework – financial, manufactured, intellectual, human, social and relationship, and natural capital – are useful for categorising the types of financial and nonfinancial value that a business should consider. To the unaccustomed reader, however, referring to the “six capitals” may sound opaque and academic. Furthermore, it may cause confusion for readers accustomed to the primacy of financial capital.

Australian integrated reporters have overcome this challenge by translating the six capitals into more accessible outcome categories. Furthermore, they often structure the contents of their integrated reports by these outcomes. As the outcomes often relate to stakeholders themselves (e.g. “employees” stand in for “human capital”), the report structure ends up speaking to the outcomes generated for each stakeholder group.

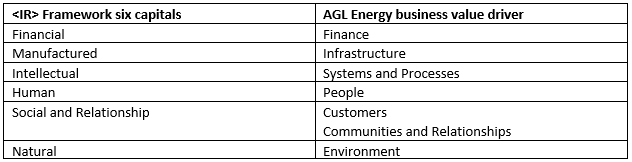

AGL Energy’s 2021 Annual Report, for example, relates their business value drivers to the six capitals as per the table below. The ensuing report structure provides a clear articulation of how the business creates value across the six capitals, thus meeting the intent of the <IR> Framework while using more everyday language.

Assurance against integrated reporting principles

Demands for independent assurance over sustainability disclosure are becoming more common, with jurisdictions such as the EU moving to require such assurance. To date, those companies obtaining independent assurance usually opt for assurance over specific data points, such as greenhouse gas emissions data or diversity breakdowns of the workforce.

Assurance of specific data points can be contrasted with principles-based assurance, which is a qualitative endeavor that seeks to confirm how a reporter has complied with reporting principles as published in frameworks such as AA1000, GRI, or the <IR> Framework itself. Select Australian examples have applied principles-based assurance to their use of the <IR> Framework:

- Stockland’s 2020 reporting was independently assured against the <IR> Framework principles of materiality, stakeholder responsiveness, reliability and completeness

- Dexus’s 2021 Annual Report was independently assured against the Content Elements of the <IR> Framework

- CPA Australia’s 2020 Annual Report was independently assured to be in accordance with the <IR> Framework in its entirety

Assurance against <IR> Framework principles can help a business confirm that the integrated reporting process is supporting integrated thinking. The <IR> Framework principles guide how a business determines material matters, how it describes its business model, and how it engages stakeholders, among other topics. Successful application of these principles requires an organisation to understand its external environment, identify factors that influence its capacity to create value (material matters) and articulate how it has incorporated these factors into its operations. Obtaining principles-based assurance not only confirms the existence of integrated thinking internally, it also sends a strong signal to the market that the business understands sustainability risks and opportunities.

Conclusion

These Australian examples are instructive because they demonstrate how companies can draw on elements of the <IR> Framework to move toward integrated thinking, no matter where they start. Furthermore, companies need not try to apply the <IR> Framework to their financial reporting immediately. There are several pathways that a company can take, including applying the <IR> Framework to voluntary reporting, as outlined in the Value Reporting Foundation’s Transition to integrated reporting: A guide to getting started.

The practices described in this article – visualizing the business model, structuring the report by value creation outcome, and principles-based assurance – could be deployed by any company looking to start its integrated reporting journey right now.

This is a blog by a guest expert. Guest expert blogs do not necessarily represent the viewpoint of the Value Reporting Foundation.